Small businesses across the Asia-Pacific can access a platform that helps them develop actionable plans to comply with sustainability standards, while enabling banks to assess and finance greener businesses, ultimately boosting sustainable trade across the region.

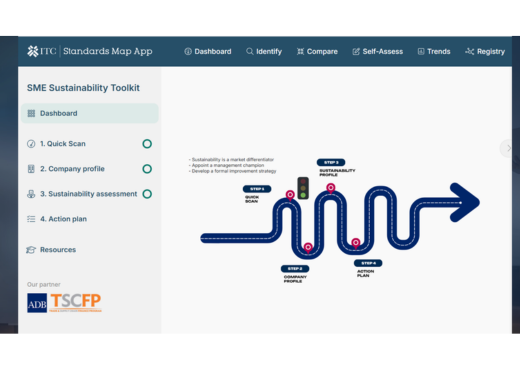

Duc Dang (Bruce), associate program officer of Trade for Sustainable Development Program of International Trade Centre (ITC), presented the Small and Medium-sized Enterprises (SME) Sustainability Toolkit, a digital tool built on ITC’s Standards Map and developed with the Asian Development Bank (ADB).

Standards Map is the world’s largest database of voluntary sustainability standards.

“The objective of the SME toolkit is to improve the company's sustainability classification, to enhance the awareness on sustainability standards, and to provide tailored recommendations for the standard compliance,” Dang said in a webinar.

He said businesses can begin navigating the toolkit https://resources.standardsmap.org/ADB-SMEToolkit/ by completing a quick scan and should answer diagnostic questions on its supply chain to help it understand what the company is doing.

“So for example, how much demand is there for product certifications (and) sustainability standards, from buyers in your industry. Do you know if your buyer is asking for any kind of certification or it is something you heard from others? Or have you heard of the standards or a requirement in the market, or have you seen any requirement in the market?,” Dang said, adding this is meant to gauge if a company needs to comply with the standards.

The ITC said the system identifies which sustainability standards are most relevant to their sector and markets, then generates a customized self-assessment and a detailed improvement plan. These plans include targeted recommendations and practical steps to help businesses strengthen areas such as environmental performance, worker safety and governance.

“The platform simplifies complex technical information and translates global sustainability frameworks into locally relevant actions,” it said.

Key features of the toolkit include artificial intelligence (AI)-assisted guidance, assess sustainability requirements against companies, certification readiness module, assess preparedness for sustainability certification, tailored recommendations, receive actionable insights to enhance compliance, interactive tools, and quick scan diagnostics and detailed reports.

Dang said the plan for the next phase is to integrate this tool as part of the financial solution.

He said commercial banks can evaluate clients –such as companies applying for loans to address gaps and meet sustainability standards– by using information from tools like Standards Map and the SME Toolkit.

“They can evaluate whether a company is ready for loans or investment, or whichever green finance that you can find. They would use this tool, integrate in the system and be able to link to the client, or to assess the client’s sustainability (performance),” he added.

Dang also underscored the need for business support organizations (BSOs) to understand the toolkit as they can also provide technical service, advisory service for companies, train them to the tool and get their information, know their gaps and take actions.

“So we have been working with ADB on the next phase of the project which will focus on this. We will disseminate the tool further, with BSO to assess or we will also work in (parallel) with financial institutions to make sure that this kind of assessment, this kind of analysis, would be used in the loan process, in making a favorable interest for company when they want to approach a loan from commercial bank in order to improve the sustainable business practices,” he said.

PHILEXPORT News and Features

Photo source: standardsmap.org

Published: March 19, 2026

Duc Dang (Bruce), associate program officer of Trade for Sustainable Development Program of International Trade Centre (ITC), presented the Small and Medium-sized Enterprises (SME) Sustainability Toolkit, a digital tool built on ITC’s Standards Map and developed with the Asian Development Bank (ADB).

Standards Map is the world’s largest database of voluntary sustainability standards.

“The objective of the SME toolkit is to improve the company's sustainability classification, to enhance the awareness on sustainability standards, and to provide tailored recommendations for the standard compliance,” Dang said in a webinar.

He said businesses can begin navigating the toolkit https://resources.standardsmap.org/ADB-SMEToolkit/ by completing a quick scan and should answer diagnostic questions on its supply chain to help it understand what the company is doing.

“So for example, how much demand is there for product certifications (and) sustainability standards, from buyers in your industry. Do you know if your buyer is asking for any kind of certification or it is something you heard from others? Or have you heard of the standards or a requirement in the market, or have you seen any requirement in the market?,” Dang said, adding this is meant to gauge if a company needs to comply with the standards.

The ITC said the system identifies which sustainability standards are most relevant to their sector and markets, then generates a customized self-assessment and a detailed improvement plan. These plans include targeted recommendations and practical steps to help businesses strengthen areas such as environmental performance, worker safety and governance.

“The platform simplifies complex technical information and translates global sustainability frameworks into locally relevant actions,” it said.

Key features of the toolkit include artificial intelligence (AI)-assisted guidance, assess sustainability requirements against companies, certification readiness module, assess preparedness for sustainability certification, tailored recommendations, receive actionable insights to enhance compliance, interactive tools, and quick scan diagnostics and detailed reports.

Dang said the plan for the next phase is to integrate this tool as part of the financial solution.

He said commercial banks can evaluate clients –such as companies applying for loans to address gaps and meet sustainability standards– by using information from tools like Standards Map and the SME Toolkit.

“They can evaluate whether a company is ready for loans or investment, or whichever green finance that you can find. They would use this tool, integrate in the system and be able to link to the client, or to assess the client’s sustainability (performance),” he added.

Dang also underscored the need for business support organizations (BSOs) to understand the toolkit as they can also provide technical service, advisory service for companies, train them to the tool and get their information, know their gaps and take actions.

“So we have been working with ADB on the next phase of the project which will focus on this. We will disseminate the tool further, with BSO to assess or we will also work in (parallel) with financial institutions to make sure that this kind of assessment, this kind of analysis, would be used in the loan process, in making a favorable interest for company when they want to approach a loan from commercial bank in order to improve the sustainable business practices,” he said.

PHILEXPORT News and Features

Photo source: standardsmap.org

Published: March 19, 2026